Read more

News

Preparing central bankers and banking supervisors for a complex world

As geopolitical tensions, climate risks, and economic fragmentation reshape the policy landscape, the Central Banking and Banking Supervision (CBBS) Programme continues to equip ESCB and SSM professionals with the knowledge, networks and perspectives needed...

It is widely acknowledged that nature-based solutions (NBS) have huge potential to support both climate change mitigation and adaptation, but our degraded nature has a limited capacity to do so. Policies such as the EU Nature Restoration Law require governments to restore ecosystems and their services, but it is questionable whether public funds alone can finance all the necessary interventions. However, the bankability of environmentally highly valuable measures such as wetland and peatland restoration is challenging for multiple reasons, in particular due to the lack of revenue from such projects.

So how could more bank (or other private) sustainable financing be unlocked? Some pieces of the puzzle are already there and others are being discussed by policymakers. First, EU regulations on ESG risk management explicitly require consideration of nature- and biodiversity-related risks and impacts. Beyond regulatory requirements, quantitative research also shows why this is important. For instance, a recent ECB working paper[1] estimates that 75% of corporate lending by eurozone banks is exposed to firms reliant on nature.

While only an indirect driver, such risk considerations can increasingly lead banks to stop financing companies with nature-degrading activities, reduce longer-term physical risks in their portfolios and even encourage supporting investments that benefit nature on the side of opportunities. Drought might be a good example of this. As water scarcity increases the credit risk of agricultural clients (and those in many other sectors), financing measures such as floodplain restoration could be seen as a way to lower risks for the sector.

Clearly, positive externalities of nature restoration and NBS might justify some targeted regulatory incentives, even prudential ones. There are countries where companies investing in nature are eligible for corporate income tax credits, and there are also examples (e.g. Hungary) of bank capital requirement reductions for loans financing such interventions.

That said, the lack of revenue generation potential of many such projects remains a major barrier. It is difficult to match the CAPEX (e.g. planning, implementation, maintenance etc.) and OPEX (e.g. monitoring, management etc. of expenses) cash flows of nature investments with ecosystem services if they remain non-monetised. Some projects may come with increased revenue opportunities through activities such as ecotourism, sustainable timber production or fisheries, but such income streams are surely not mainstream.

Furthermore, although avoiding losses can be a very important motivation for NBS, such benefits can be modelled but are still intangible and difficult to reflect in credit assessments.

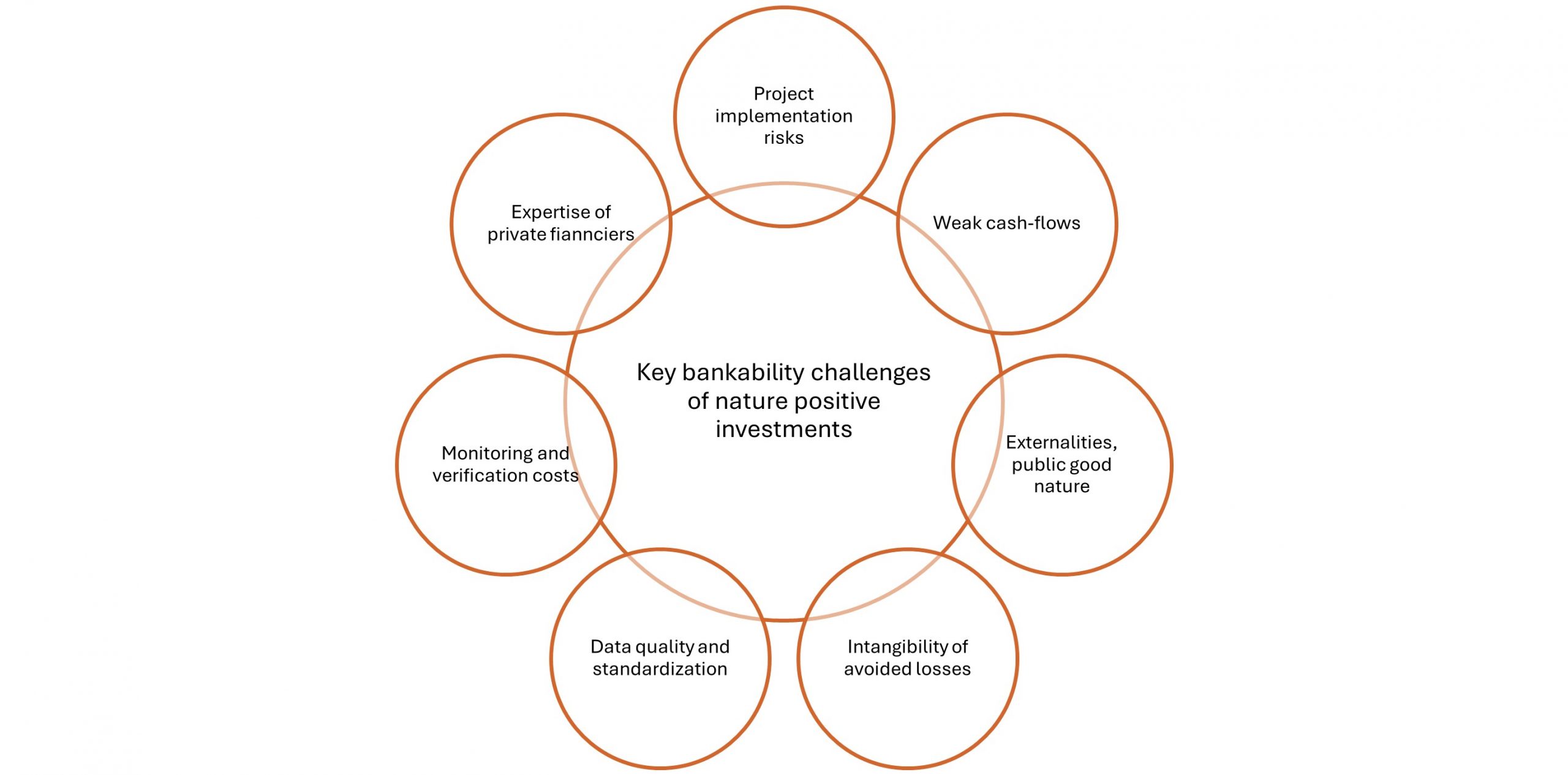

Moreover, as Figure 1 illustrates, revenue generation is only one of several bankability challenges facing nature-positive investments. Financiers must also deal with implementation risks, data challenges, public-good characteristics and verification expenses, and at the same time expand their in-house knowledge.

Figure 1: Key bankability challenges facing nature-positive finance

For the revenue challenge, carbon markets can play a role, but for many projects the key benefits are more biodiversity-related than emission-focused. Therefore, the EU plans to introduce biodiversity credits have significant potential to unlock private finance at scale. Similarly, the nature restoration plans of Member States could also play an important role by identifying funding mechanisms to mobilise private capital along with public resources.

[1] See Ceglar at al. (2025) Nature at Risk: Implications for the Euro Area Economy and Financial Stability. ECB Occasional Paper No. 2025/380, Available at SSRN: https://ssrn.com/abstract=5850073