-

Lorenzo Moretti

Research Fellow

Robert Schuman Centre for Advanced Studies

Read more

Blog

Making suptech work: evidence on the key drivers of adoption

The rapid digitalisation of financial markets is reshaping the landscape of risks that supervisory authorities must monitor and address. As data volumes grow and new threats continue to emerge, most notably ones linked to...

How can governments invest in innovative companies without distorting markets or standing back as successful companies move abroad? In Europe, this is not a theoretical question. Unlike Israel and the United States, where such interventions have been temporary, government venture capital (GVC) in Europe still anchors innovation ecosystems. As the EU steps up its technological ambitions it is important to understand the forms European GVC interventions have taken and their implications.

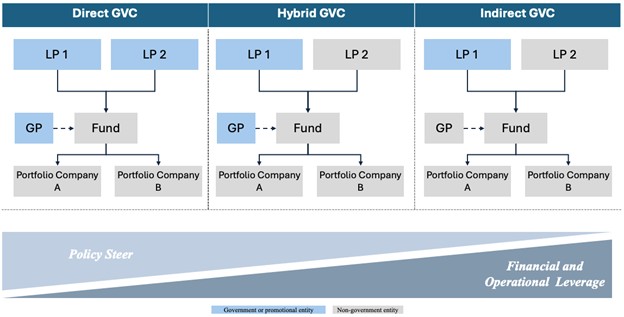

Over the past two decades, Europe has run a large-scale GVC experiment. National and EU institutions have tested and refined ways of putting public money to work in start-ups and early-stage firms, with the twin aims of supporting domestic companies and helping venture capital (VC) grow as an asset class. In this learning process three main models have emerged: direct public investment, indirect funds-of-funds, and hybrid funds. Each occupies a different position on two key dimensions that matter for policymakers: the degree of policy steer (how far governments can direct capital towards chosen priorities) and the financial and operational leverage involved in running the scheme.

Figure 1: Main Forms of Government Venture Capital Interventions in Europe

Source: author’s elaboration; also in Berger et al. 2025.

Direct GVC funds are the most hands-on. A public entity acts as both capital provider and fund manager: investment teams in public institutions invest state resources directly in companies, usually alongside private co-investors and on the same terms. This gives governments the strongest policy steer. They can prioritise sectors, technologies and regions. On the flip side, the leverage of private capital can vary significantly and it requires substantial in-house expertise to source, evaluate and manage deals post-investment.

Indirect GVC sits at the opposite end. Governments commit capital as limited partners (LPs) in privately managed VC funds, often through a ‘fund-of-funds’ model. They have no say on the selection of individual portfolio companies but can set ex ante conditions on fund governance and investment requirements. Leverage is high: relatively small public commitments can anchor much larger private funds. A lean public team oversees a broad portfolio while private intermediaries (i.e. private VC governors) do the ‘hands-on’ work.

Hybrid funds sit in between. They blend public and private (often corporate) money in vehicles managed by a public or publicly backed entity. When governance is well designed these models can combine policy steer with private-sector discipline and use corporations’ networks and expertise. The risk, instead, is that complex governance with multiple stakeholders and misaligned objectives slows decisions and dilutes investment strategy clarity.

Apart from these differences, all three European GVC models share an important feature. They deliberately replicate the classic American venture capital governance template: a limited partnership structure that separates capital providers (LPs) from specialised managers (general partners, or GPs) who manage time-limited investment vehicles (the funds). European governments have not tried to invent a sui generis ‘European’ form of venture capital. Instead, they have chosen to work with these established institutions and use public capital to spread and consolidate them across national ecosystems.

The implication is that European GVC interventions are not just a way of channelling public money into technology firms. They are a market-building strategy to strengthen VC as an asset class in a context (European financial markets) historically misaligned with it. This is why it can be an important part of both Europe’s technology strategy and the Savings and Investments Union.

Bibliography:

Beck, T., Bonaccorsi Di Patti, E., De Vincenzo, A., Guazzarotti, G., Moretti, L., Supino, I.. 2025. Financing growth and innovation in Europe: economic and policy challenges, EUI, RSC, Policy Paper, 2025/14, Florence School of Banking and Finance – https://hdl.handle.net/1814/93076

Berger, M., Criscuolo, C., Moretti, L. 2025. The Role of Public Funds to Develop the Supply of Risk Capital to Innovative Firms. Presentation at the Florence School of Banking and Finance Annual Conference, 10-11 March 2024.

Moretti, Lorenzo. 2024. Creating Innovation Markets: Government Venture Capital in Europe. published PhD dissertation.