-

Cristian Foroni

Research Associate

Robert Schuman Centre for Advanced Studies

Read more

Blog

Geopolitical risks, financial stability and central bank responses

We live in a world where geopolitical risks and geoeconomics are increasingly significant. The first 25 years of the 2000s have been marked by continual disruptions: financial shocks, anti-globalisation trends, a pandemic and geopolitical conflicts ranging from trade wars and...

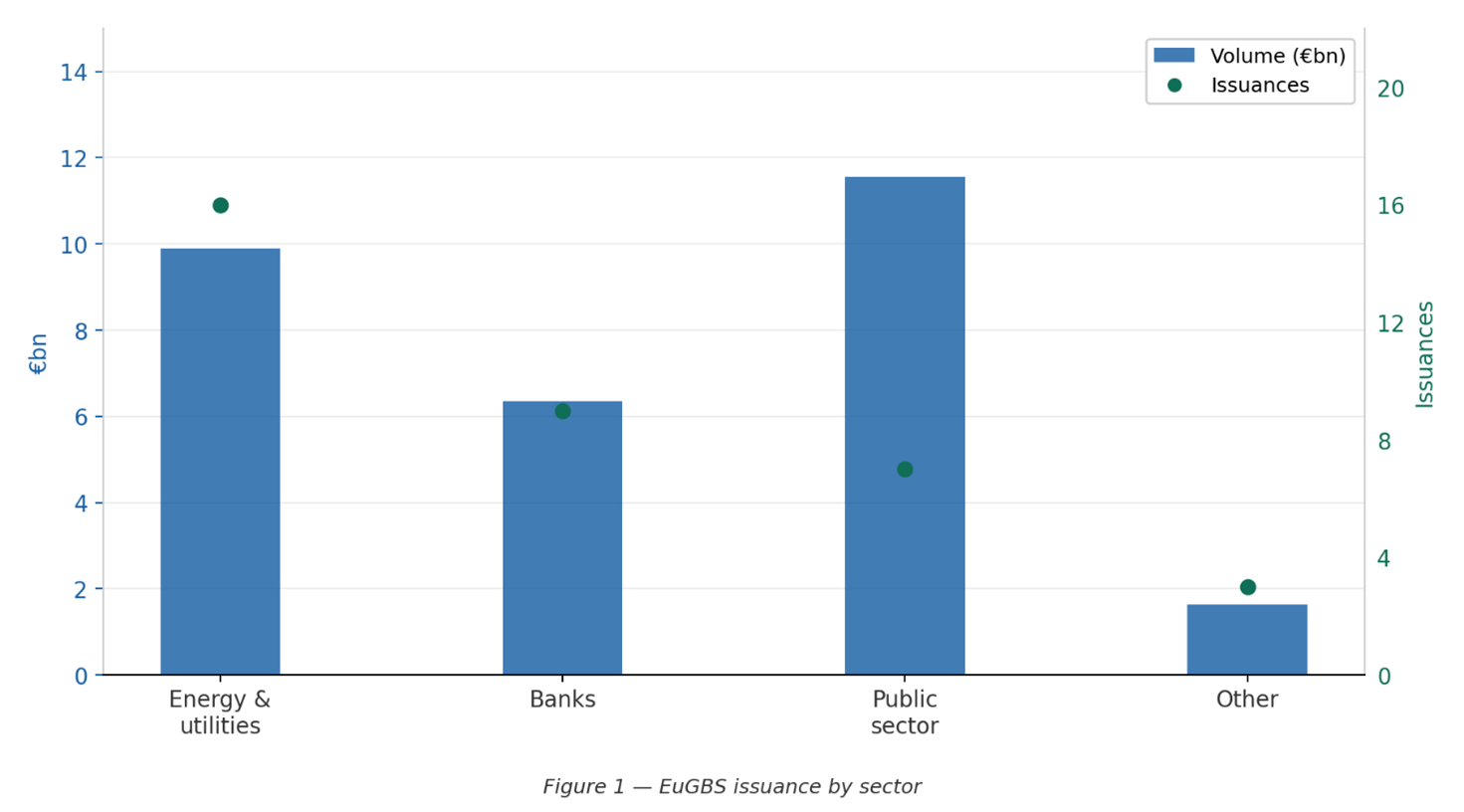

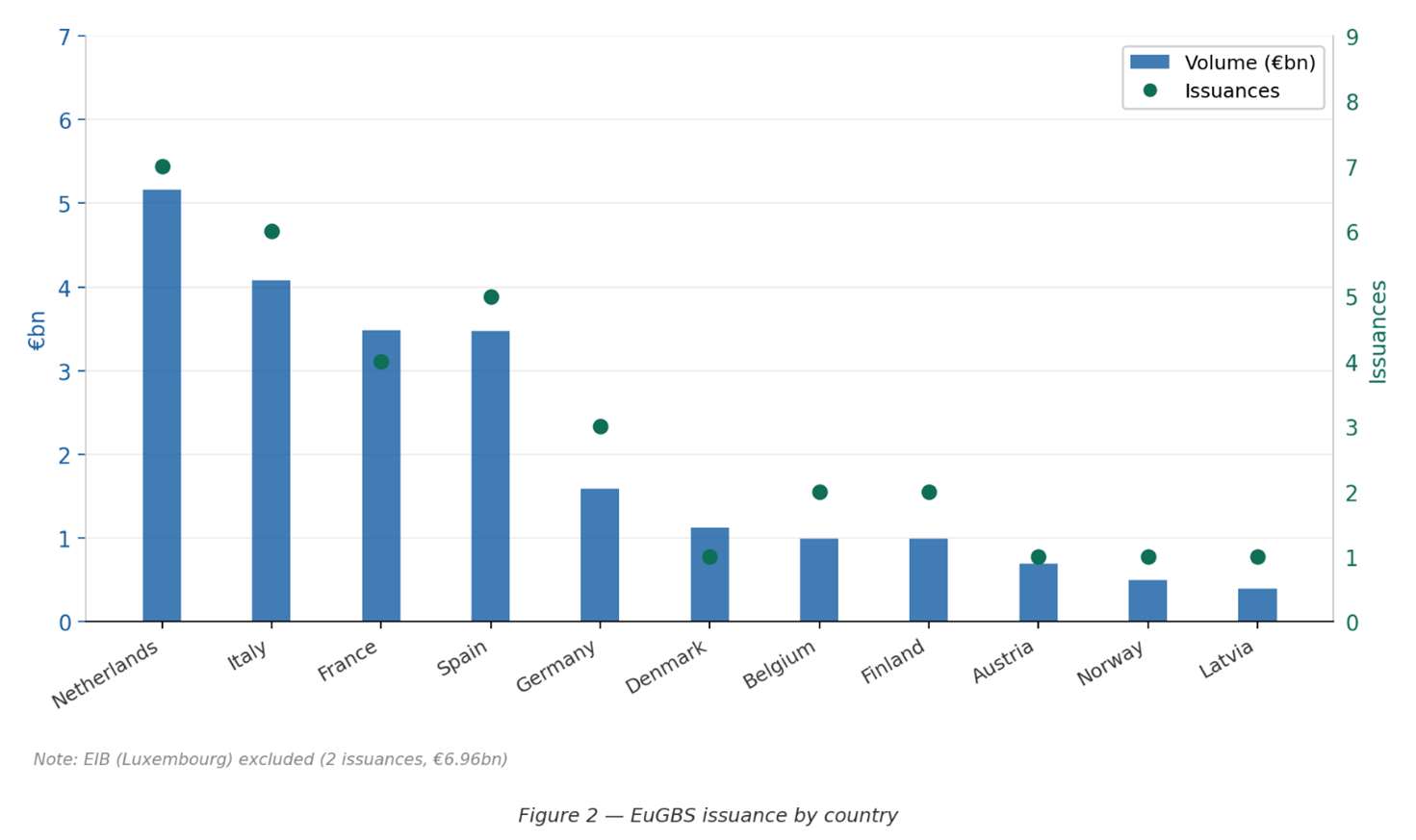

The EU Green Bond Standard (EuGBS) has now been in force for just over a year. Data available up to early April 2026 show that 35 EuGB issuances have taken place, with an aggregate volume of around €29.4 billion. By numbers of transactions, issuance is concentrated in three segments: energy and network utilities (16 transactions), banks (9) and public-sector issuers, including agencies and supranationals (7). By volume, however, public-sector issuers account for the largest share, with about €11.6 billion, followed by utilities with about €9.9 billion and banks with about €6.4 billion. The sectoral and geographical breakdown is shown in Figures 1 and 2.

To put this first year in context, it is useful to start with the problem the standard was designed to address. The case for the EuGBS rested on an intuition about how green bond markets function under voluntary regimes. When disclosure is heterogeneous and external review is recommended rather than required, investors who care about environmental integrity must undertake much of the verification themselves. Such due diligence is costly, uneven and difficult to scale up. It also weakens signalling, because issuers that incur the cost of genuine taxonomy alignment are not easily distinguishable from ones operating with looser green claims.

The academic literature on green bond pricing fits this intuition reasonably well (Kapraun et al., 2021; Pietsch and Salakhova, 2022; Fatica et al., 2021). Pricing advantages associated with green certification have not been uniform across issuers. They have tended to be stronger where credibility is already supplied by other means, particularly for governments and supranational issuers, and weaker or absent for many corporate issuers with voluntary standards. In this sense, the issue was not simply whether green bonds existed but whether markets had a credible and standardised way to differentiate stronger forms of environmental commitment from weaker ones.

The EuGBS is an attempt to change this institutional setting. Compared to traditional Green Bond Principles, it introduces a more demanding certification structure: taxonomy-based use of proceeds, mandatory pre-issuance review, mandatory post-issuance review of allocation reports and an enforceable supervisory framework. If credibility is embedded more directly in the label itself rather than left to investors to verify individually, investor-side monitoring costs should fall and the information value of issuance should rise.

The early phase of issuance is still too short to settle larger empirical questions, given the still limited number of observations. But the composition of the market is consistent with the view that first-wave issuance has come from issuers for whom the marginal cost of meeting the requirements of the standard is relatively low, reflecting in part pre-existing taxonomy alignment, issuer size and organisational capacity. Whether this pattern persists as the market develops remains to be seen. A significant regulatory threshold is 21 June 2026, when full ESMA registration of external reviewers becomes mandatory, thus ending the transitional notification regime – a development that should reduce heterogeneity in review quality and further strengthen the integrity of the certification process.

The early signals are relatively modest, but the standard is young and the market is still finding its shape. The more fundamental questions – whether enforceable certification commands a measurable pricing premium over voluntary standards, whether it changes what ultimately gets financed and what impacts can be demonstrated – will take time and considerably more data to answer. What the first year does suggest is that the EuGBS is testing an important margin: whether regulatory standardisation can make environmental credibility more legible, and therefore more valuable, in capital markets.

References

Fatica, S., Panzica, R. and Rancan, M. (2021). The pricing of green bonds: are financial institutions special? Journal of Financial Stability, 54:100873.

Kapraun, J., Latino, C., Scheins, C. and Schlag, C. (2021). (in)-credibly green: Which bonds trade at a green bond premium? SSRN Working Paper 3347337.

Pietsch, A. and Salakhova, D. (2022). Pricing of green bonds: Drivers and dynamics of the greenium. Working Paper 2728, European Central Bank.

Note: Calculations are based on available LSEG data as of 9 April 2026. Figure 2 reports the issuer domicile and excludes EIB issuance