-

Lorenzo Moretti

Research Fellow

Robert Schuman Centre for Advanced Studies

Read more

News

Teaching young women to talk about money

On 18 April 2026, the Florence School of Banking and Finance brought financial literacy to Casa delle Donne in Florence, with a hands-on workshop designed for the young women of Prime Minister Firenze — a leadership...

Should government venture capital (GVC) disappear once the industry matures? This question resurfaced in the final panel of the Florence School of Banking and Finance Annual Conference 2026 on the Savings and Investment Union (SIU), in a discussion with some of Europe’s most important promotional institutions. The default academic answer is yes (Lerner 2009). Israel’s Yozma programme has long been the classic example: the state helped create a VC industry and then stepped back as soon as it became self-sustaining (Breznitz 2007).

But in Europe the story is more complex. European VC relies on the state in part because it cannot today be anchored by Europe’s pension system. Venture capital needs large patient institutional investors willing to commit money to a risky and illiquid asset class. In the US, ‘funded’ pensions and university endowments have played this role. However, this capital base in Europe is much thinner. In particular, European pension systems are predominantly pay-as-you-go schemes: fiscal transfers between generations as opposed to personal wealth accumulation invested in various asset classes. As a consequence, pension assets in the EU amount to only about 25% of GDP (on average), compared with 147% in the US. They also allocate significantly less to VC (European Investment Bank, 2024; FIVE, 2026).

Where pension systems and other long-term investors do not supply enough risk capital, the state is the only other long-term investor that can step in to anchor the venture ecosystem. The prominence of GVC in Europe is therefore not only a result of activist industrial policy but also a response to the absence of a deeper domestic base of institutional capital. If the structure of EU pension systems does not change, neither will the structural reliance of European VC on public resources.

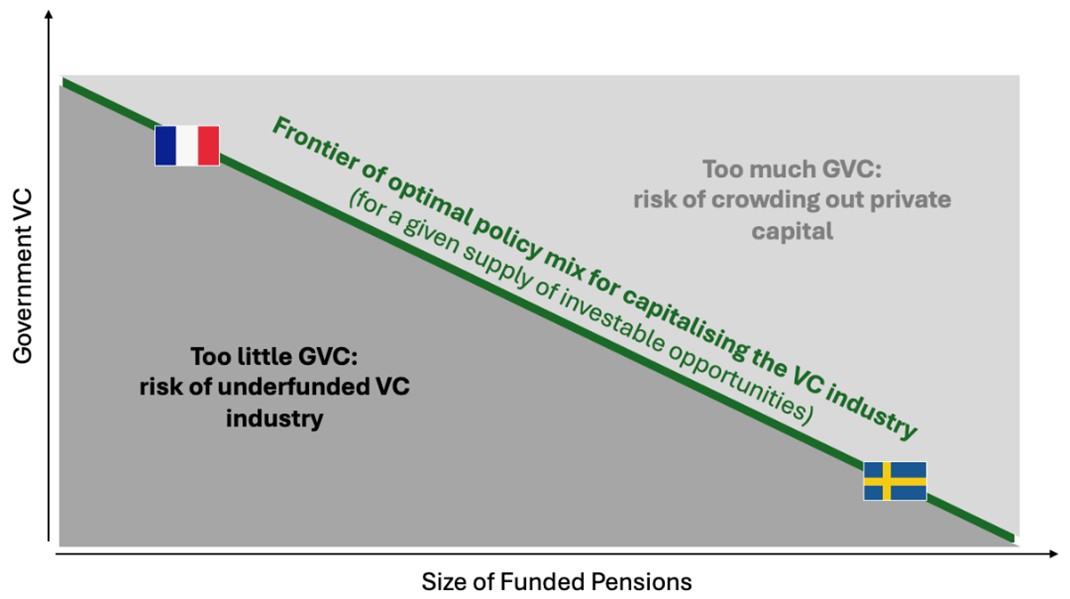

This is why, when thinking of the amount and timeline of GVC, policymakers should think in terms of a GVC-pensions equilibrium (Fig. 1). Other things being equal, for any given supply of investable opportunities there is an appropriate amount of VC. This capital can originally come from public resources, pension assets or a combination of the two (net of other institutional investors). The key point is that the ‘right’ amount of government intervention depends, in part, on the size of funded pension assets (and the extent to which they are allocated to VC).[1]

Figure 1: illustration of the GVC-pension equilibrium

This relationship transpires in policy-mix heterogeneity in Europe. In countries where funded pensions are small, the state has had to step in more prominently to help the VC ecosystem grow, as in France. In Sweden, by contrast, pension reform in the 1990s helped build funded pension assets and pension funds have become important investors in venture capital and private equity (Thomadakis, 2025). This helps explain why Sweden stands out in Europe for the strength of its VC ecosystem, despite much less visible government intervention.

Entrepreneurial and retirement (eco)systems have long been treated as unrelated policy domains. They are not. If Europe wants to rely less on GVC, it will need to build a broader base of institutional capital. In practice, this means putting pension reform and innovation finance in the same conversation. This hints at a broader point: that the complexity of the SIU agenda rests on interdependences between apparently disconnected policy domains.

Bibliography

European Investment Bank. (2024). The scale-up gap: Financial market constraints holding back innovative firms in the European Union. (European Investment Bank)

Kukies, J. & Noyer, C. (2026). Financing innovative ventures in Europe: Recommendations to close the scaleup financing gap, deepen the Savings and Investments Union and strengthen Europe’s competitiveness. German Federal Ministry of Finance. (Bundesministerium der Finanzen)

Thomadakis, A. (2025). Learning from Sweden: A blueprint for building resilient European capital markets (CEPS In-Depth Analysis). Centre for European Policy Studies. (CEPS)

[1] Note that this framework is a simplification. It ignores other sources of VC fundraising (family offices, insurance, other institutional investors) to highlight the counterintuitive policy-link between pension systems and public VC.