-

Nico Lauridsen

Research Associate

Robert Schuman Centre for Advanced Studies

-

Read more

Blog

The Peruvian paradox: How a fragile democracy built a strong central bank

The story of the Central Bank of the Republic of Peru (BCRP) stands out as one of Latin America’s quiet success stories of building strong institutions in an unstable region. This resilience is all...

The rapid digitalisation of financial markets is reshaping the landscape of risks that supervisory authorities must monitor and address. As data volumes grow and new threats continue to emerge, most notably ones linked to cybersecurity, climate change and increasingly complex digital financial activities, traditional supervisory approaches face mounting strain. In this context, supervisory technology (Suptech) has gained prominence as a key enabler strengthening the effectiveness, efficiency and responsiveness of financial oversight. Suptech consists of a wide range of digital tools, including artificial intelligence, machine learning, advanced analytics and cloud computing, which together have potential to transform supervisory practices. However, despite this promise adoption remains uneven. While many authorities have begun experimenting with these technologies, only a small subset have successfully moved from pilots to fully deployed operational systems. Understanding the institutional conditions that support or hinder this progression is therefore crucial for policymakers and researchers alike.

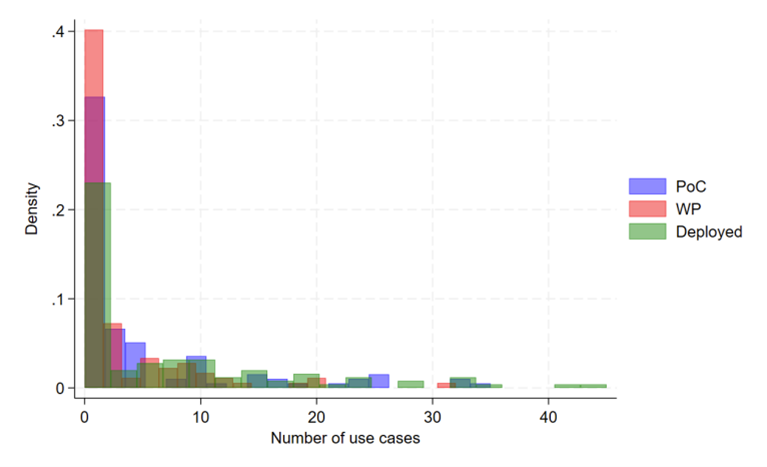

A recent study that we published as a BIS Working Paper with our co-authors Leonardo Gambacorta and Jermy Prenio from that institution addresses this question. The paper, Making SupTech Work: Evidence on the Key Drivers of Adoption, is based on the 2024 State of SupTech Survey compiled by the Cambridge SupTech Lab and DTS. The dataset contains responses from 112 financial authorities in 97 countries, thus providing a globally representative perspective that spans both advanced and emerging economies. Figure 1 illustrates the distribution of Suptech tools in the three stages of development in the Suptech lifecycle (Proof of Concept (PoC), Working Prototype (WP) and Deployed (DP)). These distributions provide a preliminary overview of the maturity of Suptech and reveal salient patterns in its diffusion across supervisory areas. In all three stages the distributions are distinctly right-skewed with a pronounced spike at zero, indicating that many authorities report no Suptech activity. The combination of excess zeros and skewed count distributions reveals a need for an empirical approach to distinguish between the decision to adopt Suptech and the extent of its implementation

Figure 1 Distribution of Suptech Activity – All use cases (Source: Cambridge SupTech Lab and DTS. Authors’ calculations.)

Findings from an analysis of SupTech adoption drivers indicate that implementing a single strategy, whether focused on digital transformation, data governance or SupTech alone, is insufficient to drive meaningful technological adoption. Authorities that integrate all three strategies deploy significantly more tools and face fewer design and implementation obstacles. Organisational characteristics also matter. Larger authorities and ones with more focused mandates are more likely to initiate advanced projects. However, establishment of a dedicated SupTech unit emerges as the strongest driver of progression from experimentation to deployment. In addition, technological enablers shape adoption patterns. Using public cloud services increases the likelihood of implementing AI tools, while reliance on in-house development is more closely associated with early-stage experimentation. Together, these results show that coherent strategies, supportive organisational structures and enabling technologies are essential to scale up SupTech in financial supervision.

Read the full article here